This post contains affiliate links.

This is my honest review of the Transferwise multi-currency account which I have been using as a freelancer based in the Netherlands. I use the Wise account for international invoices and managing some of my business finances.

Executive summary

The key benefit of using Wise for me is the ability to set up accounts in different countries and using different currencies.

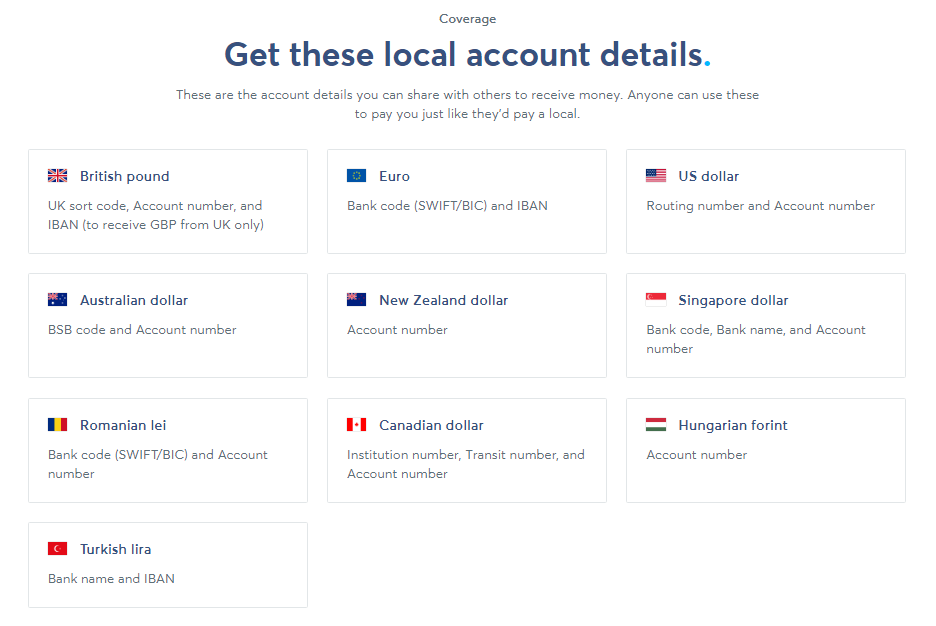

Wise allows you to set up (virtual) bank accounts in 10 currencies including Dollars, Euros and Pounds and recieve payments in these currencies.

As a freelancer in the Netherlands, the main reason I have been using the Wise account is to invoice clients in the US and UK. I can use the Wise account to set up bank details in the US and UK so that clients can pay as if to a local bank.

I can then change money at the real exchange rate, with very low fees. Wise say they are 7 times cheaper than UK banks for changing money. Read “Wise vs ABN Amro” below for a comparison between Wise and ABN Amro for international transfers.

Wise Pros & Cons

Pros

- Cheap, fast, and easy international money transfers

- Open accounts in 10 currencies, including USD, Euros, GBP

- Receive payments like a local in 10 currencies.

- Hold and convert money into 50+ currencies.

- Export CSV of transactions for accounting (or integrate with Xero / Quickbooks)

- Online payments in different currencies using Mastercard with no hidden fees

- Debit card available for offline spending in 200 countries

- Send invoices by email. Recipients just click a button to pay. They don’t need a Wise account (Business accounts only)

- No monthly fees. Accounts are free with some small additional charges

- Reasonably safe. Money held in account is kept separately from Wise should the company go bankrupt.

Cons

- Mastercard debit – not accepted everywhere in Netherlands (Maestro is used widely) but usually works online

- Not a bank account. Arguably not as safe as a Dutch bank account in that funds are not protected by a deposit protection scheme (or the UK equivalent FSCS). But see below for more on this.

- No interest. No ability to earn interest on funds

- Clients asked double-check payment details when paying. Details are flagged by their bank the first time they make the payment.

Sign up for a Wise multi-currency personal account for free – fine for freelancers, individuals or small business owners wanting to try out Wise.

Sign up for the business account – extra features for business customers such as email invoicing and batch payments to employees / contractors.

Not sure which one is best for you? Read on for more background on the personal account features, and I will cover the business account at the end.

What is Transferwise / Wise?

Wise (formerly TransferWise) is a well-known currency transfer service that is now also moving into international banking-type services in the form of multi-currency accounts.

Wise have over 10 million users worldwide for their money transfer service, a speedy and cheap way to send money across currencies at the real exchange rate with minimal fees. They also claim to have many customers using their multi-currency accounts already with £2bn in funds held.

As a business Wise is profitable and heavily backed by private investors. They are now looking to become a public company after an IPO in 2021. This is reassuring compared to some other challenger banks which are not profitable and may close down if they are not able to get another round of investment.

What is a multi-currency account?

Wise are now adding multi-currency accounts to their services. This is like a bank account that allows you to hold over 50 currencies and set up 10 virtual accounts in different currencies.

These accounts are good for freelancers (like me) taking payments from different countries.

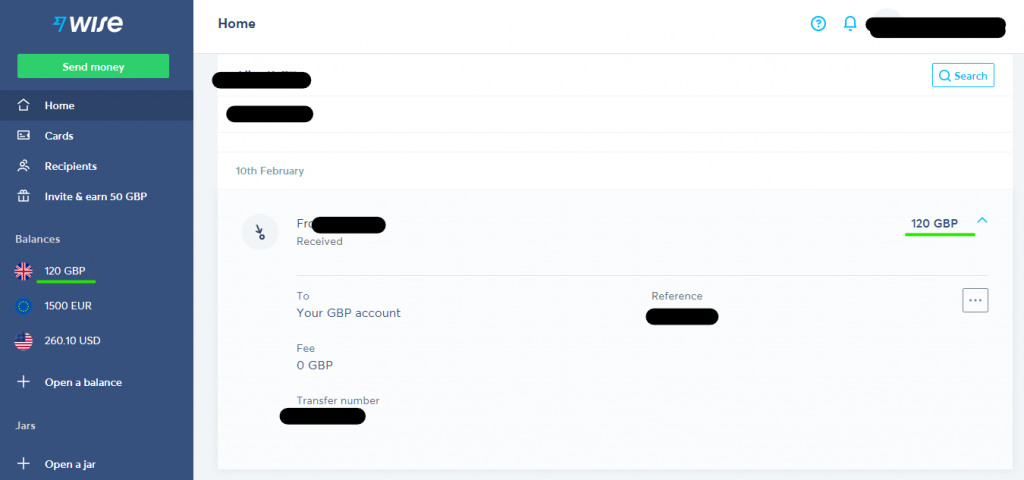

For example, I ask my clients in the UK to pay me in Pounds, to my GBP account details. They pay as if to a US bank account which is easy for them. This payment goes straight into my Wise account’s GBP balance with no fee.

I can then exchange it to Euros at the real exchange rate (with a small fee paid to Wise), or keep it as Sterling for now if I need to hold that currency.

It’s also good for expats who want to keep some money in their home currency for paying Direct Debits, bills, sending money to family / friends, or doing online shopping in different countries.

It might also be useful if your home country does not allow you to keep your bank account. However, I wouldn’t use it as a savings account as there is no interest and you actually have to pay a fee if you hold over 15k in Euros (other currencies are completely free though).

You can also use a borderless account to set up a local Euro account in the Netherlands as an alternative to a Dutch bank account. Personally I don’t do this. I have an Abn Amro account which I use for most of my day-to-day finances because the Maestro card is more widely accepted form of payment. I just use the borderless account for my business invoicing and expenses.

Is it a bank account?

No!

The Wise multi-currency account is not technically a bank account. While Wise is regulated by the FCA (Financial Conduct Authority) in the UK, this is as a payment service. Wise does not have a banking license. This means that your money is not protected by a guarantee in the same way that it would be in a UK bank for example by the FSCS scheme or a Dutch bank.

However, Wise see this as a benefit. They want to be an easier and cheaper alternative to old-school banking, especially international banking.

On top of this you can’t earn interest on your balance in the multi-currency account like with many savings accounts. However, Wise may be moving into offering investments in the future where users can potentially see returns by putting some of their balance into investments.

Is my money safe?

This is an interesting question. The short answer is yes, your money is safe because it is kept seperately in a third-party financial institution such as Barclays or JP Morgan Chase. These institutions are unlikely to go bankrupt, so the money is “safeguarded”. Wise explain their safeguarding system here.

However, Wise accounts are not bank accounts, and are not protected like British and Dutch bank accounts, which have deposit protection schemes of £85,000 and €100,000 respectively that are backed up by the government.

Using Wise in the Netherlands

Can I use the Transferwise borderless account as my local account in the Netherlands?

Yes. You can use it as you would a current account (but not a savings account!).

You can open a Euro account (based in Belgium) and get a Mastercard to pay for things online, in shops and take money out of ATMs with no fees.

However this is a Mastercard and sometimes this can’t be used as payment in the Netherlands where Maestro is universally accepted form of card payment in stores (this is because Maestro has no payment fees for store owners, unlike Mastercard and Visa).

Wise says you can also get your salary paid into the account by your Dutch employer. I think this may depend on the employer but it seems unlikely they will refuse to pay into a Belgian Euro account.

In summary there is nothing stopping you from using Wise as your sole current account for day-to-day finances.

The only inconvenience can be having to get money from an ATM when a Dutch store does not accept Mastercard (Albert Heijn!!).

Wise definitely shouldn’t be used like a savings account though. You won’t get any interest paid on your balance. Plus you have to pay 0.4% annually if you hold over 15,000 in Euros.

Do I need a BSN to open an account?

No.

This is a common problem for expats arriving in the Netherlands. How to open a bank account when you haven’t been given a BSN (Burger Service Nummer / Citizen Service Number)?

With Transferwise, the Euro account you open is based in Belgium, not in the Netherlands, and you don’t need a BSN for this.

Wise vs ABN Amro for currency transfers

Below is a quick comparison between Dutch bank ABN Amro and Wise for sending money internationally. I chose Euros to Dollars and did this on 30 March 2021.

| Provider | Amount to send | Fee | Rate (€1 =) | Cost to sender |

|---|---|---|---|---|

| ABN Amro | $1000 | €9 | .8503 | 869.69 |

| Wise | $1000 | €4.55 | .8517 | 856.30 |

Wise offers a better rate and lower fees, and is more transparent about it. Getting this information from ABN Amro wasn’t easy and the rates they show on their currency calculator are not what they offer when making a real transfer.

My personal Wise account review

My experience using the Wise multi-currency account as a freelancer / business based in the Netherlands

Pro: Invoicing abroad like a local

For me the main benefit of using this account is being able to invoice in different currencies and have clients pay as if it were to a local bank.

For example, I work with US-based clients and it is easier for their accountants to pay as if to a US account.

The first time I asked if I could be paid with Transferwise, I didn’t hear back from the client for a week. He hadn’t heard of the service, was completely confused by it, and said no it wasn’t possible. So instead I gave him the US account details I created in my Wise multi-currency account. Now he pays this way every month with no issues.

Payments are processed within a few days and I have a convenient record of all my invoices in my Wise account, which basically functions as my business bank account. I can then export this as a CSV when doing accounts and tax returns.

Pro: Save money on transfers from USD to EURO / GBP to EURO

I’ve saved €100s so far on potential fees and exchange rates that would normally be offered by traditional banks.

Pro: Useful for paying (online) business expenses (works with iDeal too)

You can also use Wise to pay business expenses, connect it to Paypal and iDeal (Dutch payment system) and use it to manage all your business finances in theory.

Con: Offline payments / card payments using Mastercard not great here in NL

In the Netherlands Maestro is widely used and Mastercard is sometimes not accepted. At the moment the only way to get a Maestro is by getting a Dutch bank account like ABN Amro or ING.

In addition to this, there is a 1.75% fee for ATM withdrawals over £200 each month. In other words free ATM withdrawals are limited to £200 each month. I am not sure what this limit is in Euros as it isn’t listed on their website.

The Wise business account

Benefits of the business account vs personal

The business account is great for startups, entrepreneurs and ambitious freelancers. As a freelance sole-trader with no employees I have yet to make full use of the features available to business customers (but I’d like to someday).

Key benefits of the business account vs personal:

- Pay up to 1000 employees in bulk internationally (great for distributed teams if you hire a virtual assistant or a team of developers)

- Pay invoices with the real exchange rate

- Invoice with an email sent to an email address (no bank details needed from them)

- Get debit cards for your team and create different accounts for different teams / personel

Full features of the business account can be seen on the Wise business accounts page here.

Business or personal?

The business account is free to set up (or you deposit a small amount to get some features like Direct Debits and the ability to recieve payments) so you can try it out. If you are a growing business with a few employees and international customers it could be really useful. It depends on your business needs.

However, the personal account is also free and works for me as a freelancer working with a manageable number of clients.

To sum up…

In summary, my experience with this account has been great as a small freelancer working with international clients. It allows me to invoice clients in local currency and I have a record of the amount in Euros and USD or GBP that I can easily export and add to my accounting when I submit my accounts.

I’ve saved hundreds on exchange rates and fees that I would have paid with conventional banking and transfers between international clients.

The speed and reliability of payments has been good.

The main drawback from a Dutch-based expat is the lack of Maestro card but that’s ok for me as I also have a Dutch bank account.

I’m interested to see what happens next with Wise as they plan to issue an IPO in 2021. There are also rumours of allowing users to create investment pots so they can potentially earn returns (or losses!) on the money held in a Wise multi-currency account.

I want to know in case some bidy is depositing money in my wise card, are these money going to be watched by the tax collecter or outkarey?

Really helpful article! Do you also pay fees to transfer money from Wise into your Dutch bank account?

Hi!

Thanks for the helpful article. Quick question. if you receive money from a US client in an account that resides in the US (before using Wise to transfer the balance to GBP/EUR), does that have a VAT implication for you in the US? Will the US tax authorities see it as a domestic service and want to deduct VAT on it?

Thanks!

Ark

Hi Ark. Great question! I had not thought about this.

I found the following in Wise’s help articles but the example given is Germany (for a UK customer) not the US:

Q: If I open a EUR account (through the German bank, Deutsche Handelsbank) do I need to submit a tax declaration in Germany? Or pay any German tax on my balances?

A: The Wise account itself will not create a taxable presence (commonly referred to as a permanent establishment). Assuming you have no other assets or activity in Germany, you will have no tax obligations including German tax return filings.

Link: https://wise.com/help/articles/2932394/how-does-tax-work-with-my-wise-account

Perhaps the same can be said for the US. The Wise account is not a “taxable presence” as they say. After all these accounts actually belong to Wise rather than being under your name, as I understand it.

Thanks for the question.